With global warming and the issue of climate change continuing to intensify, countries' awareness of carbon reduction has steadily increased. In December 2015, the 195 member states of the United Nations signed the Paris Agreement (COP21). The agreement established the following targets to be achieved before the end of the 21st century, collectively aimed at curbing the global warming trend:

1. Limit global warming to between 1.5°C and 2.0°C

2. Reduce carbon emissions by 50% by 2030

3. Achieve net-zero emissions* by 2050

*Net-zero emissions, also known as "net zero," refers to the quantity of greenhouse gas emissions that are directly and indirectly caused globally by companies and organizations within a specified time period and that are offset to net zero after various energy saving and carbon reduction measures.

Carbon emissions were the primary cause of global warming and climate change. The combustion of fossil fuels was the main source of carbon emissions, and fossil fuels served approximately 80% of global energy demand. Given the current population growth trajectory, global energy demand is projected to increase at least 50% by 2050. Unless the critical changes occur in energy production and consumption, this anticipated increase in energy consumption will result in higher carbon emissions. In view of this, Delta formed a new business unit, HEBD, for hydrogen business development in 2022. Delta HEBD signed a technology license agreement with Ceres Power in 2024 and formally commenced the development of fuel cell and electrolysis solutions offering new options for energy generation and consumption.

International decarbonization pathways and the importance of hydrogen energy

The IEA (International Energy Agency) released "Net Zero by 2050: A Roadmap for the Global Energy Sector" report which analyzes the development of low-carbon technologies and indicates that hydrogen and carbon capture, utilization, and storage (CCUS) are the ultimate means for the world to achieve Net Zero. Reviewing global development trends, the IEA projects that by 2050 total hydrogen demand will exceed 530 million metric tons per year, with demand for clean hydrogen reaching 388 million metric tons per year. Hydrogen is expected to be applied primarily in three sectors: industry, transport, and power generation.

Hydrogen can be used as fuel and generate power by combustion or by fuel cells, during which no carbon emissions occur. For industrial sector, the carbon emission can be reduced by blending hydrogen into natural gas as combustion fuel or deploying fuel cell systems in office buildings, manufacturing plants, and data centers as stable, standalone sources of clean electricity. In transportation sector carbon emission reducing, administrators can promote Fuel Cell vehicles and synthetic fuels (e-Fuel) to replace using liquid fuels. The power generation sector primarily relies on renewable electricity to reduce carbon. The electrolysis-produced hydrogen can be integrated into renewable energy systems to manage the seasonal and intermittent variability issue in the coming future.

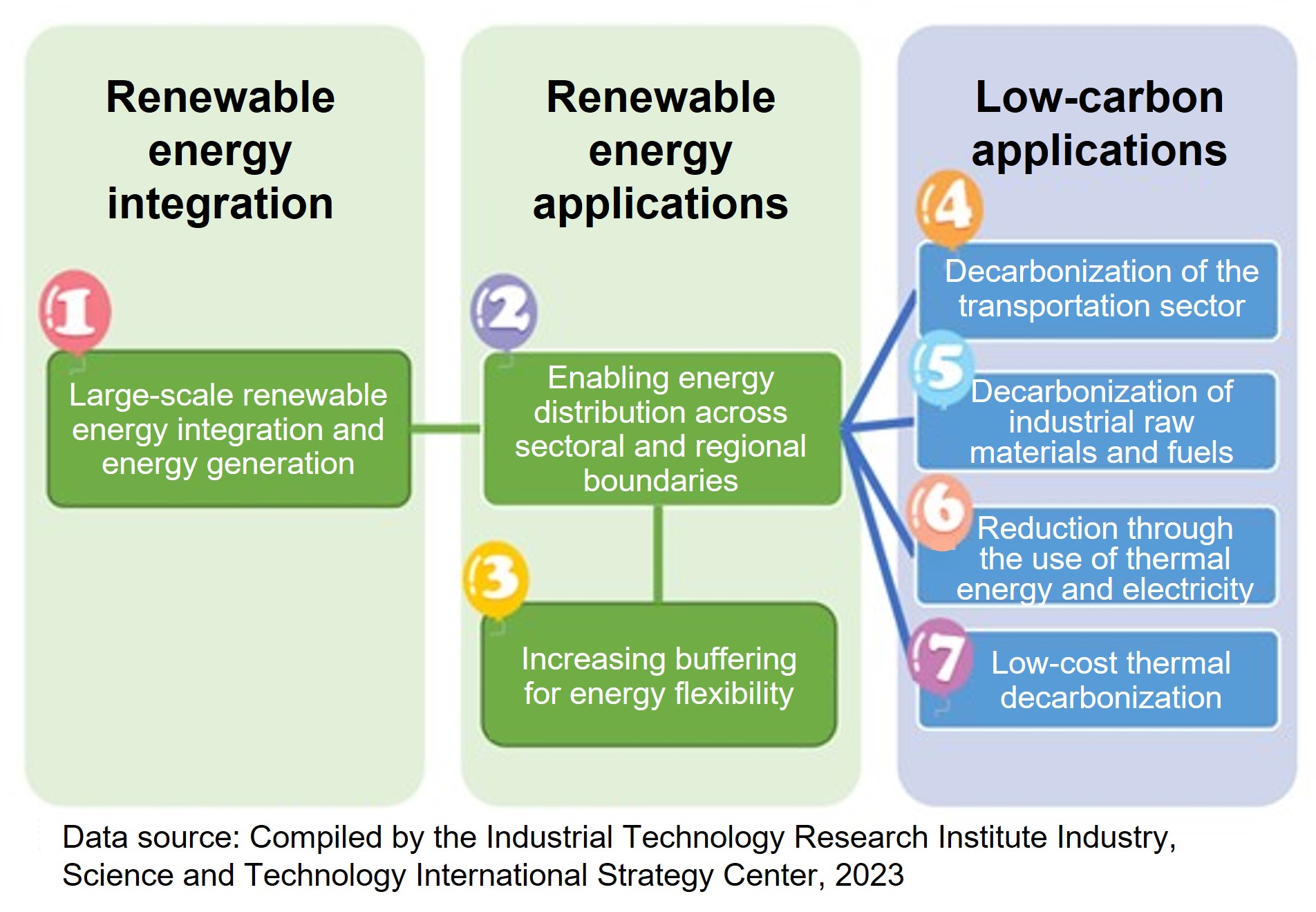

The seven roles of hydrogen in the energy system

Dynamic scan for global major markets

KPMG indicated that more than 130 countries worldwide have announced 2050 net zero commitments and actions to provide industry a clear net zero pathway and accelerate emission reduction. Since 2020, many countries have begun to formulate hydrogen development strategies and have allocated funding to subsidize hydrogen infrastructure research and industrial cluster project development. As implementation policies and detailed rules for low-carbon hydrogen certification criteria, tax credits, and CFD (Contract For Difference) Strick Price take shape, related subsidy programs have begun to materialize and initiated low-carbon, clean, and green hydrogen production subsidy auctions or bidding processes. Examples include the EU’s European Hydrogen Bank, the UK’s hydrogen allocation rounds, and 2nd round of H2 Global bidding in Germany.

The World Hydrogen 2025 Summit was the leading annual event for the global hydrogen industry. The exhibition attracted participants from over 120 countries and more than 700 hydrogen companies, spanning key nodes across the entire hydrogen industry value chain including government, hydrogen production development, equipment supply, financing for investments, infrastructure and end applications. IEK analysts noted that, based on discussions at the event, the hydrogen industry has been gradually moving from the earlier “vision phase,” which focused on policy declarations and technological breakthroughs, into a “commercialization phase” centered on business models. The industry has shifted from the stages of “technological breakthroughs,” “policy commitments,” and “carbon reduction benefits” toward considerations of “market demand formation,” “project investments being realized,” and “the establishment of long-term business models.”